The $529 Billion Wedge: Prescription Drugs Deep Dive

Edition 7: Unpacking the Most Actionable Lever in U.S. Healthcare

Trendline Health | Edition 7 - February 4, 2025

Bending the Trendline: Unpacking the forces driving disruption in U.S. healthcare, one category at a time.

Quick Take: Drugs as the Healthcare Wildcard

In 2025, prescription drugs accounted for $529 billion, or 9.4%, of total NHE, growing faster than hospitals (6.8% YoY) and physicians (5.9% YoY) amid demand for weight-loss and oncology therapies. This stabilized from the 2023 GLP-1 spike, but volatility keeps drugs as the “tip of the spear.” With biosimilars advancing, Mark Cuban-style disruptors, and fresh 2026 congressional scrutiny of vertical integration, drugs remain the battleground for transparency and affordability.

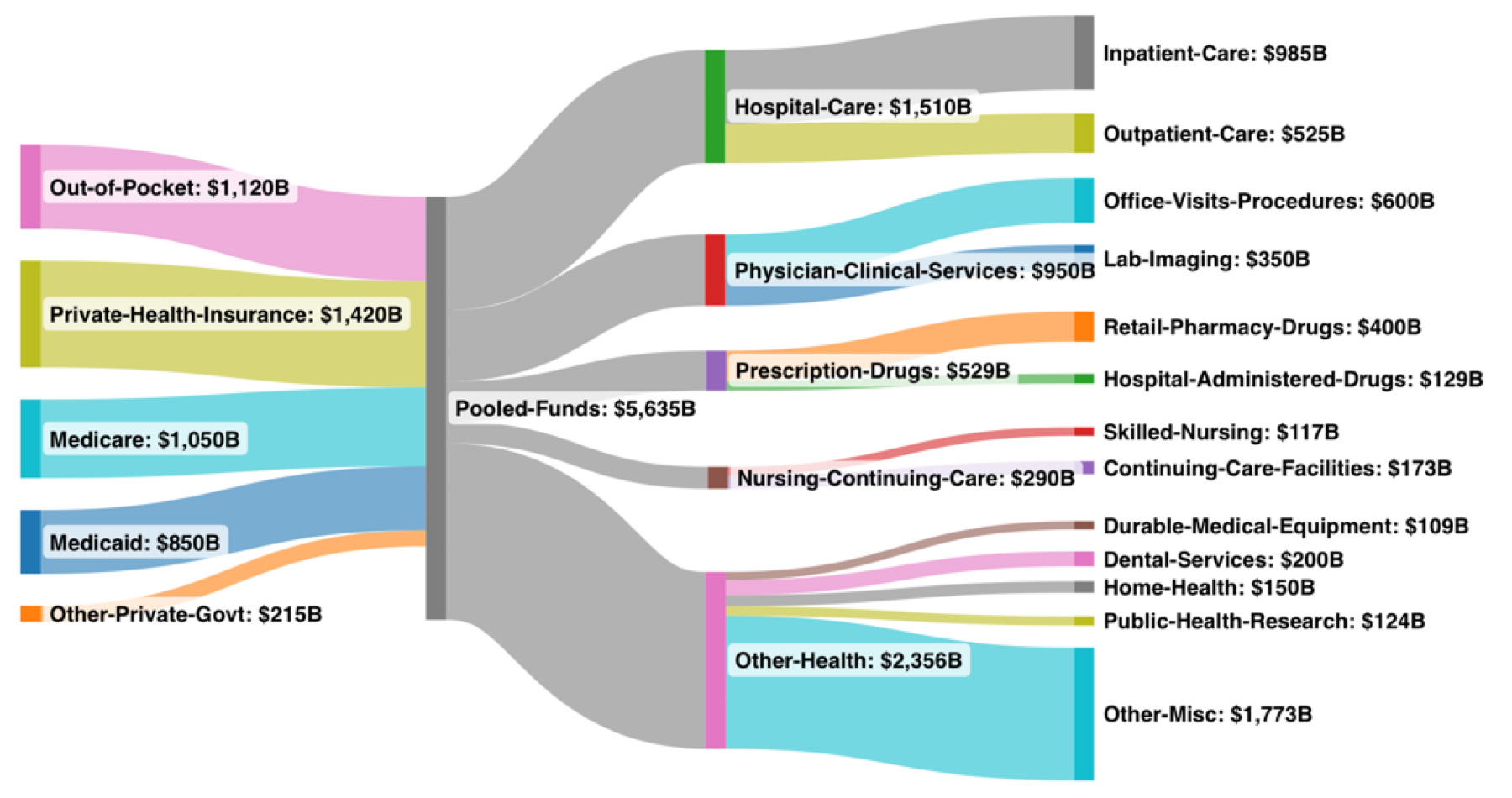

$5.6 Trillion National Health Expenditure

Inflows and Outflows (billions)

As noted in Edition 6, total NHE hits ~$5.6T in 2025 per CMS June 2025 figures, still tracking closely in early 2026 updates.

The 2025 Numbers in Context

CMS places 2025 NHE at $5,635B (consistent with Edition 6), drugs at 9.4% (~$400B retail, ~$129B hospital/Part B). Drugs trail hospitals ($1,510B, 26.8%) and physicians ($950B, 16.9%) but lead nursing care ($290B, 5.1%). The ~7% YoY drug growth (aligning with CMS 7.1% overall NHE) is fueled by innovation yet tempered by IRA caps and generics. Medicare covers ~30% (6% growth), while private plans face 10.2% inflation—hitting employers hardest.

Understanding the Ecosystem: The Rise and Role of Pharmacy Benefit Managers (PBMs)

PBMs evolved from 1960s claims processors to rebate-negotiating powerhouses. The Big Three (CVS Caremark, Express Scripts/Cigna, OptumRx/UnitedHealth) control >80% of prescriptions.

This vertical integration creates the closed-loop profit engine highlighted in Edition 6, owning payer, negotiator, dispenser, and often provider, fueling opacity and steering.

Trendline Health adaptation mapping Big Three consolidation across the drug channel, illustrating the ~80% control flagged in Edition 6.

PBMs claim cost reductions via negotiations, but critics cite spread pricing, rebate retention, and artificial hikes (per 2024 FTC report). Vertical steering raises antitrust flags, echoed in January 2026 House hearings grilling execs on steering and costs. Backlash includes 2025 FTC suits, state RICO filings, transparency bills, and 2026 bipartisan pressure on affordability/prior auth. Employer surveys show 80% view drug volatility as top concern, making 30%+ PBM margins untenable.

Disruptors Enter the Fray: Mark Cuban’s Cost Plus and the Push for Transparency

Mark Cuban’s Cost Plus Drugs bypasses PBMs with transparent pricing (cost +15% + $3 fee), boasting 500,000+ users and $1B in claimed savings by 2025 via direct sourcing and 50-80% cuts on generics/biosimilars. Cuban calls PBM deals “racketeering,” amplifying RICO threats and ERISA audit urges. This inspires pass-through models and government integrations, signaling systemic momentum.

Policy Meets Disruption: Trump RX and the Most-Favored-Nation Push

Trump’s “Trump RX” (May/September 2025 EOs) pushes MFN pricing for Part B drugs and direct discounts via TrumpRx.gov. Pharma partnerships target 80% cuts on chronic meds, projecting $20B savings by 2027. Cuban praises it as countering PBM monopolies, though legal challenges persist. January 2026 testimony amplified momentum with transparency calls and pledges like UnitedHealth ACA rebates.

Why Drugs Are the Tip of the Spear for Healthcare Disruption

Drugs highlight innovation vs. opacity: gene therapies deliver miracles at high costs, visible via copays/premiums. Biosimilars (20+ in 2025-2027) could shave 30% off biologics; IRA expands negotiations. But AI-personalized meds risk 15%+ spikes by 2030. Watch employer carve-outs and RICO waves as change signals.

Bending the Trendline: Five Stories Defining Early 2026 Momentum

These developments build on 2025’s foundation, showing real potential to alter the $5.6T trajectory in 2026 and beyond.

PBM Transparency Gains Momentum Post-January Hearings – Bipartisan Capitol Hill scrutiny of PBM/insurer execs yielded pledges (e.g., UnitedHealth rebates) and faster adoption of transparent alternatives (up sharply from 2025 levels). This could deliver $10-30B in near-term relief via full pass-throughs and bans, extending Edition 6’s reform acceleration.

Most-Favored-Nation Drug Pricing Expands with Pharma Agreements – Late 2025/early 2026 deals with 9-14 major pharma firms align U.S. prices closer to global benchmarks for Medicaid/cash-pay, with pushes to codify legislatively. Early estimates: $15-25B savings by 2027-2028, amplifying Trump RX impact.

Biosimilar Uptake Accelerates, Pressuring Biologics – 20+ launches/gains in late 2025/early 2026, plus formulary shifts and IRA expansions, position biosimilars to cut 25-35% off key categories, redirecting billions and easing premium pressures.

AI-Driven Efficiencies Scale System-Wide – Beyond 2025 pilots, wider AI rollout (ambient documentation, predictive analytics) targets >15% readmission drops and growing admin savings. Forecasts suggest this offsets 8-9% medical trends, helping curb overhead nearing $600B.

Employer-Led Shifts Intensify Cost Containment – With projected 7.6-9% 2026 trends, more carve-outs, direct models, and site-of-care steering pressure hospitals/insurers on value, potentially slowing price inflation in the 26.8% hospital slice beyond PE slowdowns.

Stay tuned for Part 2: Hospitals in our series.