Hospitals: The $1.6 Trillion Immovable Object

Trendline Health | Edition 8

Trendline Health | 2026 | Edition 8

Quick Take: Hospitals as the Core Cost Driver

Hospitals remain the largest single slice of U.S. health spending—~31% in 2024—and drove 40% of national health expenditure (NHE) growth from 2022-2024 ($277B of $692B total increase, per KFF Feb 2026 analysis). While drugs grab headlines for volatility, hospitals’ steady, massive scale (post-COVID utilization rebound + price acceleration) makes them the “immovable object” in affordability debates. Amid bipartisan scrutiny of nonprofit tax-exempt status and calls for site-neutral reforms, hospitals face pressure to justify their share of the $5.3T+ system.

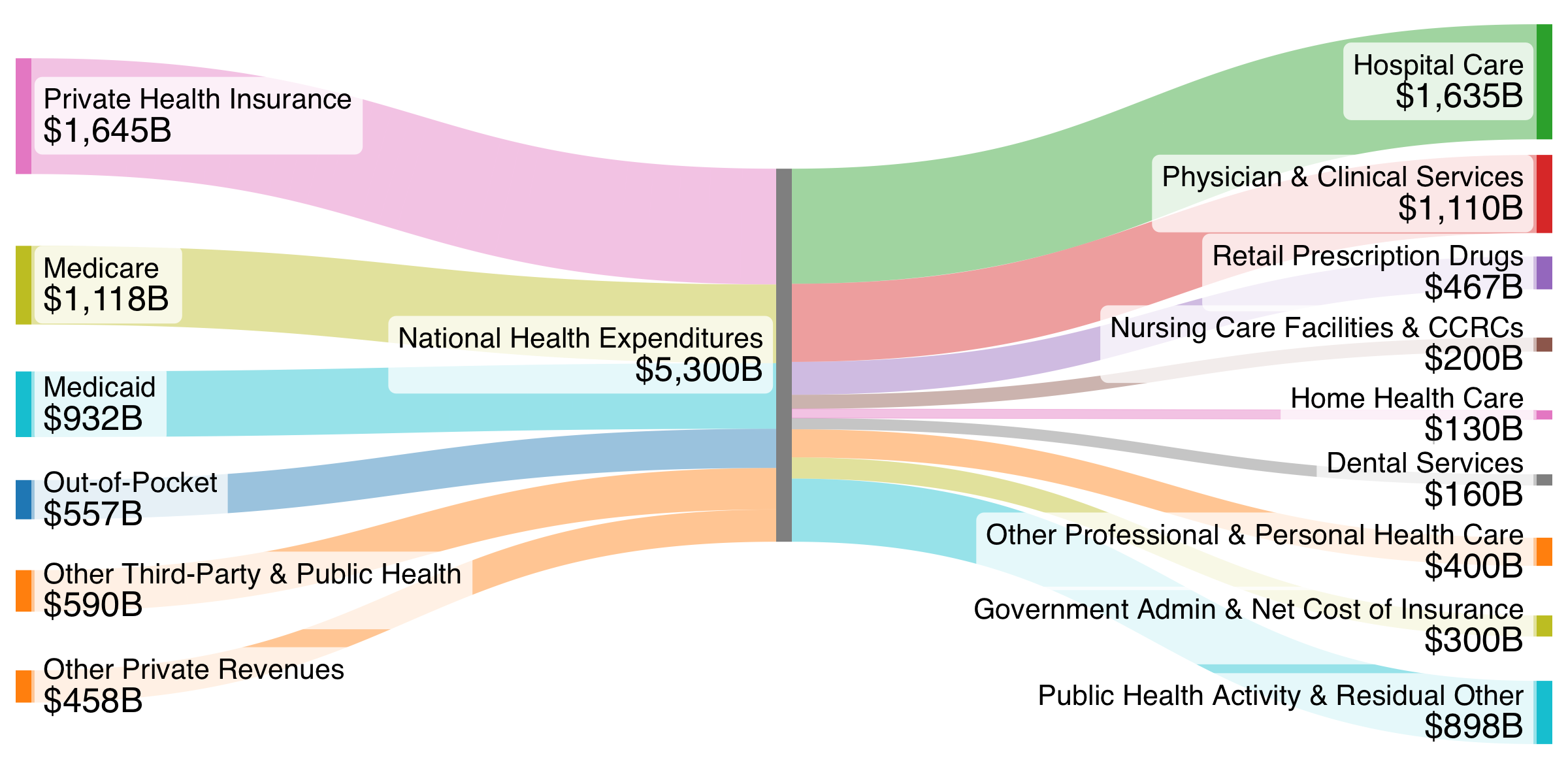

$5.3T+ Trillion National Health Expenditure (Updated)

Source: Trendline Health visualization based on CMS NHE (latest 2024 actuals + projections). Hospitals now ~$1.635T in 2024 (31%), up from earlier estimates. Edition 6 projected ~$1.51T for 2025; 2024 actuals hit $1.635T (8.9% growth), aligning with rebound trends.

The Recent Numbers in Context

Per KFF (Feb 11, 2026) and CMS data: NHE rose from $4.6T (2022) to $5.3T (2024), +$692B. Hospitals contributed $277B (40%), far outpacing physician/clinical (22%), drugs (11%). Hospital growth: 10.6% (2023) and 8.9% (2024) vs. overall 7.4%/7.2%. Drivers: Post-COVID rebound in use/intensity (outpatient visits +44% long-term) + prices (3.4% in 2024, fastest since 2007). Commercial prices grew faster than Medicare/Medicaid.

Long-term (2005-2024): Hospitals +$1T (from $609B to $1.6T), 32% of total NHE growth. GDP share: 4.7% → 5.6% (projected 6.4% by 2033). CMS projects hospitals hold ~32% growth share through 2033, with NHE to $8.6T and 20.3% GDP.

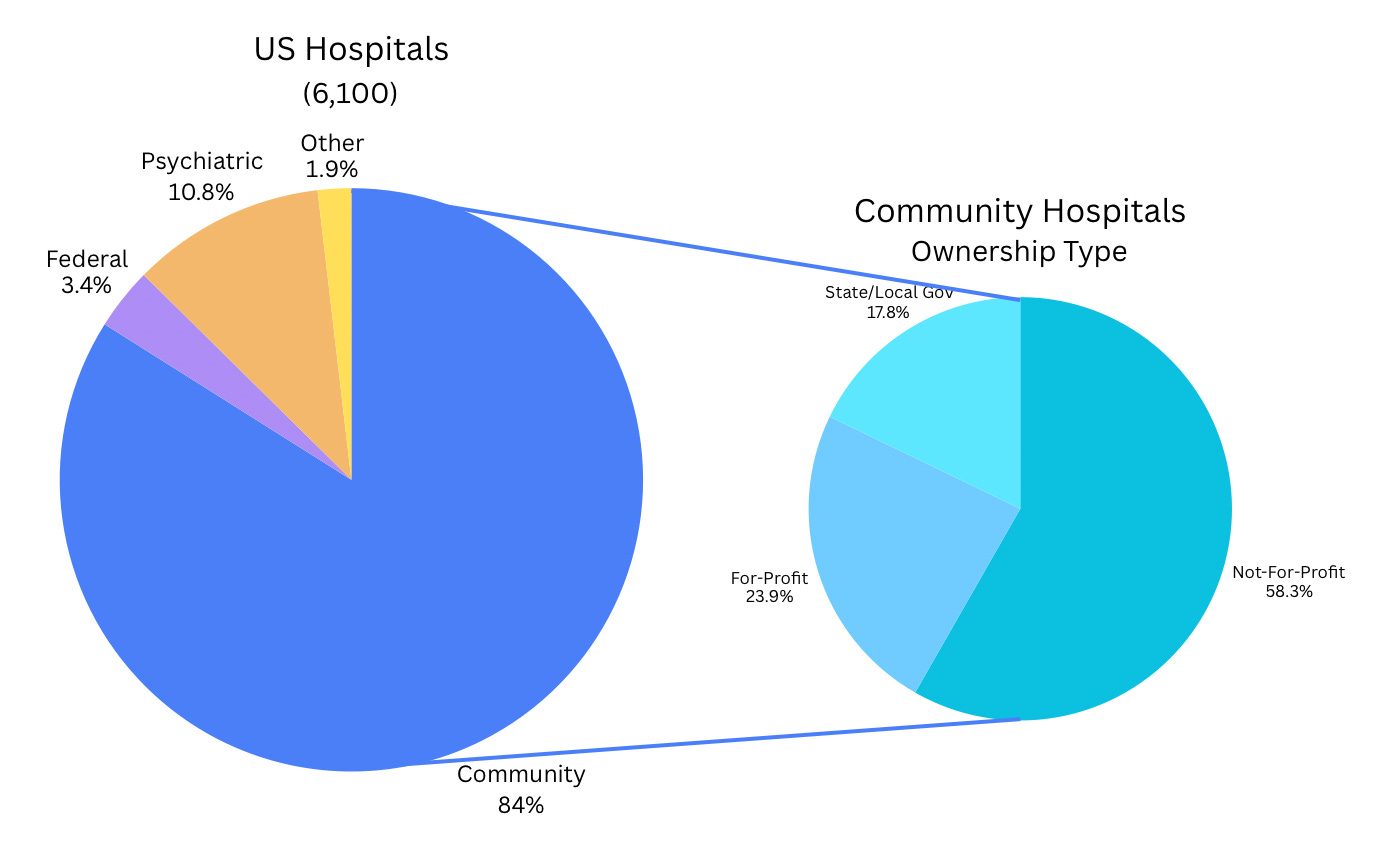

Understanding the Hospital Ecosystem: Consolidation, Nonprofit Model, and Scrutiny

Hospitals consolidated heavily pre-2025 (Edition 6 noted PE slowdown via FTC blocks). Nonprofit status dominates (~60% of hospitals), granting tax exemptions (~$13-37B annually) in exchange for “community benefits” (charity care, Medicaid shortfalls, education/research).

Current backlash: 2025 House hearings scrutinized if benefits match exemptions. Some studies show $149B benefits vs. $13B exemptions (11:1 ratio per AHA/EY 2026), but critics (GAO, Families USA) highlight low charity care relative to tax breaks, aggressive billing/debt pursuit for eligible patients, and “mission drift” toward profits. Bipartisan calls for clearer standards, more oversight, or reforms (e.g., revoke exemptions for low charity providers). Vertical integration (hospitals owning clinics/physicians) drives steering and higher prices, echoing PBM issues.

Why Hospitals Are the Immovable Object for Disruption

Hospitals embody entrenched economics: High fixed costs, essential services, limited substitutes. Growth from outpatient shift + price leverage (especially commercial) pressures premiums/employers. Nonprofit scrutiny adds political heat—potential site-neutral payments or tax changes could shave billions but risk access in rural/underserved areas.

Stay tuned for Part 3: Physician Consolidation in our series.

Bending the Trendline: Five Stories Defining Early 2026 Momentum

Building on Edition 7, these hospital-focused developments show potential shifts:

Site-Neutral Payment Reforms Gain Traction – Momentum from 2025 reconciliation/bills pushes Medicare alignment across sites, potentially curbing $10-20B+ in outpatient inflation.

Nonprofit Tax-Exempt Scrutiny Intensifies – Post-hearings, proposals for stricter charity care minimums or reporting; could redirect billions if exemptions tied to performance.

Rural Hospital Aid and Closures Watch – Reconciliation funds ($50B over 5 years) aim to stabilize, but margins remain thin (2-7%); preventing waves of closures bends access/cost curves.

AI and Operational Efficiencies Scale in Hospitals – Beyond diagnostics, AI for revenue cycle/readmissions yields 10-15% savings pilots; wider adoption could offset labor/supply inflation.

Employer/Plan Steering to Lower-Cost Sites – With 7-9% trends, more carve-outs/direct contracts bypass high-cost hospitals, pressuring consolidation and pricing.